For years, insurers have handled Scope 3 reporting the same way most large organizations have: report the categories that are easiest to measure, fill the remaining gaps with spend-based estimates, and treat claims-related emissions as too fragmented to track accurately.

The proposed 2026 Phase 1 updates to the GHG Protocol change that approach significantly.

In our previous article on the GHG Protocol’s 2026 Phase 1 revision, we covered the 95% coverage threshold and the requirement to separate primary data from secondary estimates. That conversation raised a follow-up question we have heard repeatedly from sustainability and claims teams: how do we actually know where our data sits on the quality spectrum?

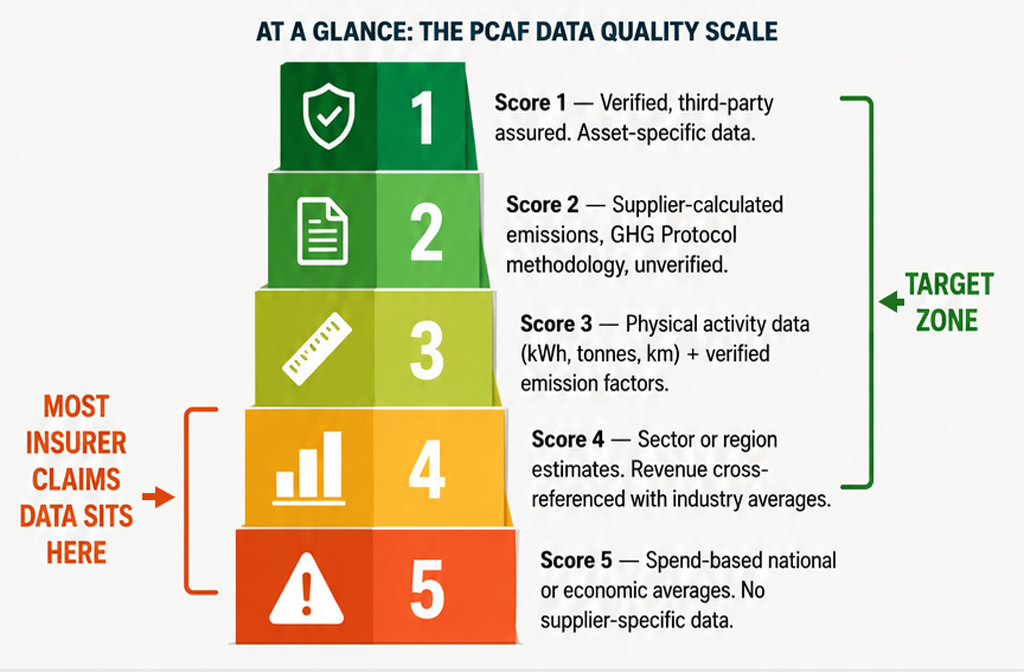

The Partnership for Carbon Accounting Financials (PCAF) answers that question with a five-tier data quality score, where 1 represents the strongest verified data and 5 represents broad sector or economic estimates. PCAF released the third edition of its Global Greenhouse Gas Accounting and Reporting Standard in December 2025, expanding coverage to new asset classes and tightening expectations for Scope 3 reporting.

For insurers, this matters because PCAF scoring is increasingly used as the underlying assessment behind disclosures filed under IFRS S2, OSFI B-15, and CSRD. A high proportion of Score 4 and Score 5 data does not just look weak in a disclosure document. It is becoming a measurable signal of reporting risk.

Score 1: Verified emissions data directly from the supplier or asset, third-party assured.

Score 2: Unverified emissions data calculated by the supplier following GHG Protocol methodology.

Score 3: Activity-based data using physical units (kilowatt-hours, tonnes, kilometres) combined with verified emission factors.

Score 4: Estimated emissions using sector or region-specific data, often supplier-reported revenue cross-referenced with industry averages.

Score 5: Estimated emissions using national or economic-activity-based factors, typically derived from spend data alone.

The closer a data point sits to Score 1, the more defensible it is during audit and the lower the uncertainty range around the reported number.

Claims supply chains are fragmented across thousands of restoration contractors, materials suppliers, equipment rentals, and waste haulers. Most insurers calculate Category 1 emissions by multiplying claims spend by a sector-average emission factor. That is, by definition, a Score 5 calculation.

The GHG Protocol’s proposed 95% coverage threshold does not directly require Score 1 data. It does, however, require companies to disclose how emissions were calculated and whether they were verified. When disclosure separates primary from secondary data, a portfolio dominated by Score 4 and 5 estimates becomes visible to anyone reviewing the report.

That visibility is the point. Disclosure rules are not asking insurers to be perfect on day one. They are asking insurers to be honest about where the data is weak and to have a credible plan to strengthen it over time.

The path from Score 5 to Score 3 or better is not theoretical. It involves four practical shifts:

PCAF scoring is the quiet infrastructure underneath every Scope 3 disclosure an insurer files. The 95% rule did not invent this scoring system, but it made the gap between Score 1 and Score 5 a lot harder to hide.

EcoClaim TRAX™ Emissions Reporting applies PCAF and TCFD-compliant attribution methodologies directly to the claims supply chain, helping insurers move from spend-based Score 5 estimates toward activity-based Score 3 data and beyond. Learn more at ecoclaim.ca/ecoclaim-trax-emissions-reporting.

Learn more: https://ecoclaim.ca/trax

Pathzero documentation — PCAF data quality scale, updated 2026 → https://docs.pathzero.com/en/improving-data-quality-from-pcaf-5-to-1

Arbor.eco — PCAF v3 Guide (December 2025 release), December 15, 2025 → https://www.arbor.eco/blog/the-guide-to-the-partnership-for-carbon-accounting-financials-pcaf

StepChange — How Data Quality Works Under PCAF, July 2025 → https://www.stepchange.earth/blog/how-data-quality-works-under-pcaf-the-foundation-of-credible-financed-emissions-reporting

Sprih — Financed Emissions PCAF Guide 2026, March 18, 2026 → https://www.sprih.com/blogs/financed-emissions-pcaf-guide-for-banks-2026/